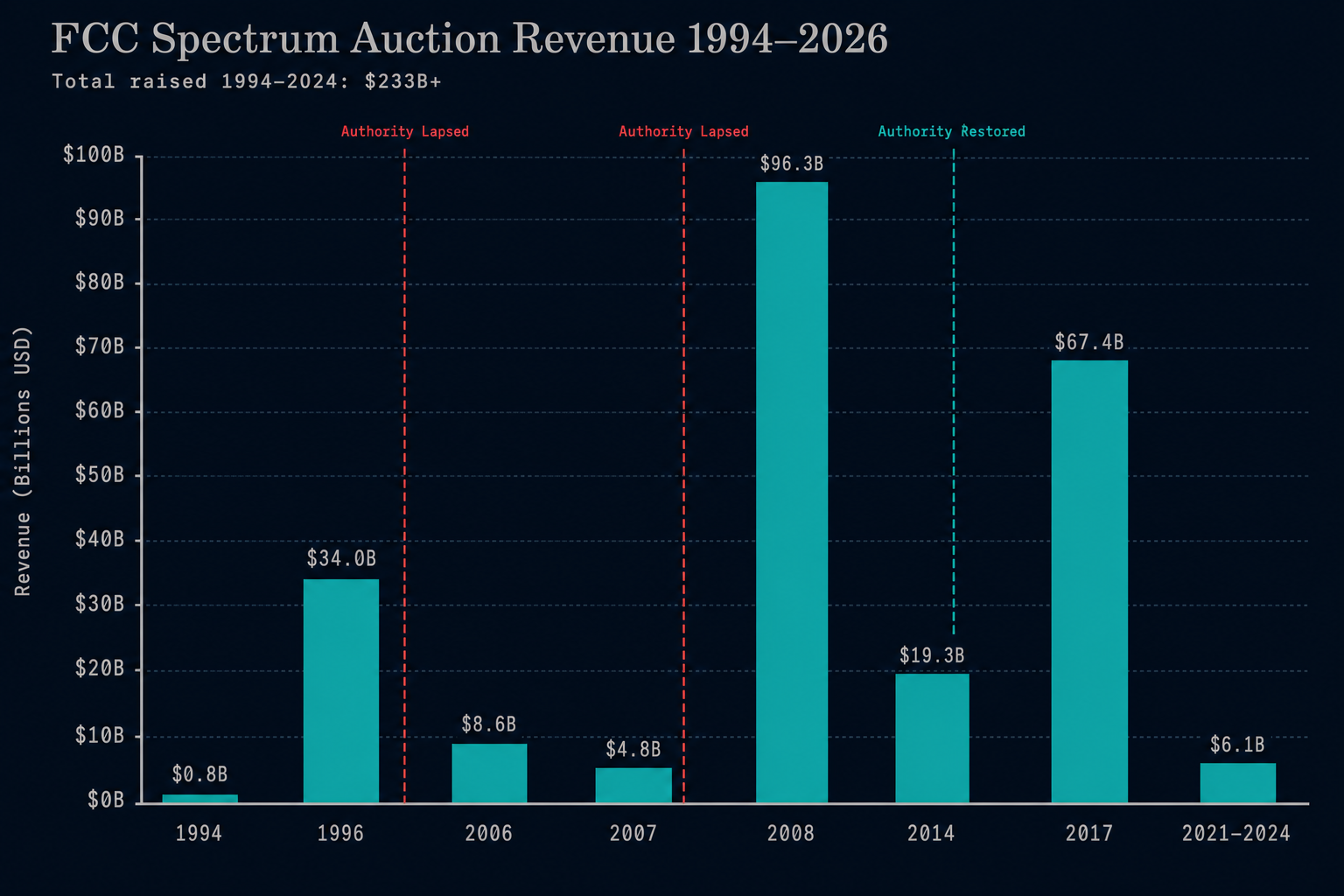

The Federal Communications Commission has conducted spectrum auctions under 47 U.S.C. § 309(j) since July 1994, using competitive bidding to assign commercial licenses across dozens of frequency bands. Since that first narrowband PCS auction, the FCC has held more than 100 auctions raising over $233 billion for the U.S. Treasury. Auction authority lapsed March 9, 2023 and was restored July 4, 2025.

How FCC Spectrum Auctions Work

The FCC’s statutory authority to conduct competitive bidding derives from Section 309(j) of the Communications Act of 1934, as amended by the Omnibus Budget Reconciliation Act of 1993. The provision directs the Commission to use competitive bidding when mutually exclusive applications exist for spectrum licenses, a mechanism Congress chose explicitly to maximize economic efficiency and revenue recovery for the public fisc.

The standard auction format is the Simultaneous Multiple-Round Ascending (SMRA) auction. All licenses in a given auction are open for bidding simultaneously. Rounds proceed in discrete intervals, typically 30 to 90 minutes: during which qualified applicants submit bids on individual licenses. The high bidder at the close of each round holds “provisionally winning” status. Bidding continues until no new bids are submitted in a complete round across any license.

Activity rules govern participation throughout. Under the FCC’s eligibility framework, a bidder must maintain a specified activity level, measured in megahertz-pops (MHz-pop), the product of licensed bandwidth and covered population, relative to their declared upfront payment. Bidders who fail to meet the activity threshold face automatic reductions in eligibility for subsequent rounds. This rule prevents bid shielding and strategic holdout behavior. The Commission calculates MHz-pop eligibility from upfront payments filed in Form 175 applications.

The Commission also employs minimum opening bids and reserve prices. Minimum opening bids are set at a per-MHz-pop rate determined by the Bureau’s economic analysis team, reflecting recent comparable auction prices, propagation characteristics, and population densities. Reserve prices, below which the FCC will not award a license: have been applied selectively; the 2020 C-band auction (Auction 107) carried no reserve price, while earlier PCS auctions used band-specific minimums.

Winning bidders have 10 business days after auction close to remit full payment. Failure to pay results in license cancellation, re-auction, and a default payment obligation, typically a percentage of the bid amount plus the difference between the defaulted bid and any lower re-auction price. Build-out and coverage obligations attach post-grant, with Commission-specified milestones at three, five, or ten years depending on license tier.

A Brief History of FCC Spectrum Auctions (1994–2024)

Congress granted auction authority in 1993 after earlier comparative hearing and lottery systems proved inefficient and susceptible to legal challenge. The FCC’s first auction, Auction 1, the Nationwide Narrowband PCS auction, ran July 25–29, 1994, covering ten licenses and generating $617 million in gross bids across 47 rounds. That inaugural event drew six bidders and established the SMRA template.

The Broadband PCS A and B Block auction (Auction 4) followed, running December 5, 1994 through March 13, 1995. The auction raised $7.7 billion over 112 rounds, assigning licenses in 51 major trading areas for the 1850–1910 MHz and 1930–1990 MHz bands. The C Block auction ran December 1995 through May 1996 and added another $13.4 billion in gross bids: though subsequent financial defaults by NextWave Wireless triggered years of litigation and forced the Commission to re-auction recovered licenses.

The Advanced Wireless Services-1 (AWS-1) auction (Auction 66) in 2006 cleared 1710–1755 MHz and 2110–2155 MHz for $13.7 billion. Auction 73, the 700 MHz auction of January–March 2008, assigned licenses in the 698–806 MHz band and raised $19.592 billion. That auction introduced open-access conditions on the C Block, enforceable under 47 C.F.R. § 27.16, after Google and public interest advocates lobbied the Commission in Docket GN 06-157. Verizon won the majority of C Block licenses subject to those conditions.

The AWS-3 auction (Auction 97) of November 2014 through January 2015 produced $44.9 billion in gross bids, the record at the time, across 1695–1710 MHz, 1755–1780 MHz, and 2155–2180 MHz. AT&T and Verizon together accounted for the bulk of winning bids. Congress had directed that AWS-3 proceeds fund the First Responder Network Authority (FirstNet) construction.

Auction 1001, the broadcast incentive auction: ran March 2016 through March 2017. It was the world’s first two-sided incentive auction: a reverse auction paid television broadcasters to relinquish 600 MHz UHF spectrum, while a forward auction sold repurposed licenses to commercial bidders. The auction repurposed 84 megahertz of spectrum, generating $19.8 billion in total proceeds. T-Mobile spent approximately $8 billion to acquire 600 MHz licenses that now undergird its nationwide low-band 5G network.

Auction 107, the C-band auction, ran December 8, 2020 through February 17, 2021, offering 280 megahertz in the 3.7–3.98 GHz band across 5,684 Partial Economic Area licenses. Net proceeds totaled $81.1 billion. Verizon bid $45.5 billion (56 percent of total), AT&T spent $23.4 billion, and T-Mobile committed $9.3 billion. The auction stood as the largest gross-proceeds auction in U.S. spectrum history. A class of incumbent satellite operators, Intelsat, SES, and Eutelsat, received accelerated relocation payments totaling approximately $9.7 billion to vacate the lower 300 MHz of the band by December 2021.

Following the March 2023 lapse of the FCC’s Section 309(j) authority, the first lapse in the program’s 30-year history: no new auctions commenced. CTIA estimated the gap cost the U.S. economy access to 100 MHz or more of mid-band spectrum that carriers needed to sustain 5G capacity. The authority gap closed when President Trump signed the One Big Beautiful Bill Act on July 4, 2025, restoring the FCC’s general auction authority through September 30, 2034.

Key Auction Types: Incentive, Clock, Combinatorial

The FCC employs three principal auction designs, each suited to different spectrum repurposing scenarios. Understanding the mechanical differences matters for policy analysts tracking proceeding timelines and bidder strategy.

The incentive auction format, codified in Section 6402 of the Middle Class Tax Relief and Job Creation Act of 2012 (Public Law 112-96), involves a three-stage process. In Stage 1, a reverse auction determines the aggregate cost to clear a target amount of broadcast spectrum by soliciting voluntary relinquishment bids from television licensees. The Commission runs successive “clearing rounds” reducing the target until gross forward auction proceeds exceed reverse auction clearing costs plus relocation expenses. In Stage 2, the forward clock auction assigns the repurposed spectrum to commercial bidders. In Stage 3, an assignment phase allocates specific frequency ranges to forward auction winners. The 2016–2017 incentive auction required four clearing-target stage attempts before closing.

The ascending clock auction (ACA) format, used in Auction 107 and the upcoming Auction 113, proceeds through sequential rounds in which the bidding system announces per-block prices for each spectrum category in each Partial Economic Area. Bidders submit quantity demands at the announced prices. When demand equals supply in all categories across all service areas, the auction closes. The format reduces exposure risk, the danger that a bidder wins licenses in some markets but not others, rendering the incomplete set strategically valueless, because prices rise gradually and bidders can calibrate demand responses each round.

The combinatorial clock auction (CCA) structure, used extensively by Ofcom in the United Kingdom and the Canadian Radio-television and Telecommunications Commission (CRTC) in Canada, allows bidders to submit package bids on combinations of licenses. The FCC studied CCA design in Docket WT 05-211 but has not adopted it for domestic auctions, citing implementation complexity and the risk of computationally intractable winner-determination problems at scale. CTIA and AT&T have each filed comments opposing CCA adoption; T-Mobile’s record in that docket was more neutral. The Commission’s Office of Economics and Analytics concluded in a 2005 staff analysis that the SMRA format remained preferable for the size and heterogeneity of U.S. spectrum markets.

A fourth variant, the modified second-price auction used in the assignment phase of incentive auctions: functions as a sealed-bid Vickrey-style mechanism. Winning bidders pay prices reflecting the displacement costs imposed on other bidders by their frequency-specific preferences, not their own bid amounts. The mechanism encourages truthful preference revelation for specific frequency positioning within an already-assigned geographic license.

The Spectrum Pipeline: What’s Left to Auction

The available commercial spectrum pipeline depends on both FCC-managed non-federal bands and NTIA-coordinated federal-use reallocation. The two agencies operate under a Memorandum of Understanding dating to 2010 that establishes joint coordination protocols, though decision authority on federal spectrum reallocation rests with NTIA under 47 U.S.C. § 902.

The Biden administration’s National Spectrum Strategy, released November 13, 2023, directed NTIA to identify at least 1,500 MHz across federal and mixed-use bands for in-depth study. The Strategy flagged more than 2,700 MHz for broader analysis, including the 3.1–3.45 GHz, 5.03–5.091 GHz, 7.125–8.4 GHz, 18.1–18.6 GHz, and 37.0–37.6 GHz ranges. Completion of band-specific studies was projected over a 3–5 year horizon. The Biden National Spectrum Strategy carries significant implications for upcoming proceedings and the overall reallocation timeline.

The most immediately actionable pipeline item is the Upper C-band (3.98–4.2 GHz). The One Big Beautiful Bill Act directs the FCC to auction at least 100 MHz in this band within two years of July 4, 2025. The Commission’s Office of Economics and Analytics has stated it does not anticipate Upper C-band bidding beginning before September 30, 2026, given incumbent fixed satellite service coordination requirements.

The AWS-3 Auction 113 is the near-term certainty. Bidding is scheduled to commence June 2, 2026. The auction covers 200 licenses in the 1695–1710 MHz, 1755–1780 MHz, and 2155–2180 MHz bands. The Congressional Budget Office estimated Auction 113 proceeds at $3.3 billion over the 2025–2034 budget window; independent analysts have modeled a range of $3 billion to $4.5 billion. Surplus proceeds above $3.3 billion would fund $280 million for regional technology hubs, with the remainder directed to deficit reduction.

NTIA’s first formal band nomination for reallocation under the new authority was 1.675–1.680 GHz. The agency also disclosed four bands under active study: 1.680–1.695 GHz, 2.7–2.9 GHz, 4.4–4.94 GHz, and 7.125–7.4 GHz. Each band involves federal agency coordination, principally with the Department of Defense, National Oceanic and Atmospheric Administration (NOAA), and NASA, and carries timelines of two to seven years before commercial licenses could reach auction. The $42.5 billion BEAD broadband deployment program operates on a parallel track; the BEAD program’s infrastructure funding interacts with spectrum availability in the 900 MHz and 2.5 GHz bands used for fixed wireless access.

Policy Tensions: DoD, Commercial Carriers, and NTIA

The central fault line in U.S. spectrum policy runs between the Department of Defense’s need for exclusive, interference-free access to mid-band frequencies and commercial carriers’ demand for contiguous mid-band spectrum to sustain 5G capacity. The 3.1–3.45 GHz band sits at the center of this dispute.

DoD systems in the 3.1–3.45 GHz range include shipborne and ground-based radar platforms that cannot tolerate interference from high-power commercial base stations. The Pentagon has consistently opposed commercial reallocation of the lower 3 GHz band on national security grounds, a position it reiterated in responses to the 2023 National Spectrum Strategy consultation. The One Big Beautiful Bill Act reflected DoD’s position by excluding the 3.1–3.45 GHz band in its entirety from the auction pipeline, with band studies not due until October 2026.

A competing proposal, advanced by AT&T and reportedly supported by DoD during 2025 deliberations: would move Citizens Broadband Radio Service (CBRS) Tier III users from the 3.55–3.7 GHz band into the lower 3 GHz range, freeing the CBRS band for re-auction as exclusive high-power 5G spectrum. WISPA and rural fixed-wireless operators strongly oppose this restructuring, arguing it would strand existing CBRS infrastructure investments. Ten Republican Senators wrote FCC Chairman Brendan Carr in September 2025 to preserve CBRS rules as-is, citing rural broadband service continuity.

NTIA’s role as coordinator for federal spectrum use creates structural latency in the reallocation pipeline. Unlike the FCC, NTIA does not adjudicate by formal rulemaking with notice-and-comment timelines. Band studies can take years; NTIA has no statutory obligation to complete them within a fixed period absent specific Congressional direction. The Department of Defense and NTIA completed their study of the Lower 37 GHz band in November 2024, paving the way for a co-equal shared-use framework, but that process began in 2023. The 3.1 GHz and 7/8 GHz band studies received approved funding in early 2025; final reports are not due before late 2026.

Commercial carriers, AT&T, Verizon, and T-Mobile, collectively representing the CTIA position in most filings, have argued before the Commission that delays in mid-band reallocation directly constrain 5G network investment. CTIA’s economic modeling, filed in WT Docket proceedings, projects that each year of delay in clearing 100 MHz of mid-band spectrum costs the U.S. economy approximately $100 billion in foregone productivity. The figure is contested by DoD and by public interest groups that argue interference modeling understates risk to defense radar systems. The ORAN security debate adds another layer of complexity to the infrastructure investment calculus, intersecting with spectrum policy at the network architecture level.

The FCC itself has limited direct authority over federal frequency allocations: its jurisdiction under the Communications Act covers non-federal spectrum. The Commission can influence the interagency process through formal recommendations to NTIA and through its own proceeding record, but cannot compel DoD to vacate bands. This jurisdictional split has been a recurring subject of Congressional oversight hearings and is embedded in the structural tension between the Spectrum Pipeline Act of 2015 and subsequent legislative proposals.

What’s Next: Upcoming Spectrum Proceedings

Several proceedings are active or imminent as of early 2026. Policy analysts and industry counsel should track the following dockets and deadlines.

Auction 113 (AWS-3), Bidding opens June 2, 2026. Competitive bidding rules were published in the Federal Register on August 4, 2025 (90 FR [Docket AU 25-119]). Filing requirements and upfront payment procedures were published December 23, 2025. The FCC expects 200 licenses to be contested; AT&T and T-Mobile are considered the principal bidders given their existing AWS-3 license gaps from Auction 97.

Upper C-Band Proceeding, The Commission has an OBBBA-imposed statutory deadline of July 2027 to initiate the Upper C-band (3.98–4.2 GHz) auction. A Notice of Proposed Rulemaking establishing auction procedures is expected in late 2025 or early 2026. Satellite operators that hold incumbent rights in the 4.0–4.2 GHz range will require coordination under Part 25 of the FCC’s rules prior to license grant.

CBRS Band Restructuring, No formal rulemaking has been initiated as of the article date. The AT&T/DoD proposal to migrate CBRS Tier III users and re-auction the 3.55–3.7 GHz band for exclusive high-power use remains in informal comment stage. The FCC’s Wireless Telecommunications Bureau has not issued a public notice opening a record. If a proceeding is initiated, it would carry a minimum 90-day comment cycle before any proposed rules could be finalized under Section 553 of the Administrative Procedure Act.

37 GHz Shared-Use Framework: Following the November 2024 DoD-NTIA band study, the FCC is expected to open a rulemaking establishing co-primary government-commercial rules for the 37.0–37.6 GHz band. The band is relevant for fixed wireless access backhaul and mmWave 5G, though propagation characteristics limit its utility for wide-area mobile coverage. Licensing rules have not been proposed.

Spectrum Fees Study, Congress directed NTIA and FCC to conduct a joint study on the feasibility of spectrum use fees for federal agencies, due 18 months after enactment of the One Big Beautiful Bill Act—approximately January 2027. Industry groups including CTIA have opposed extending fee structures to commercial licenses; the study scope is limited to federal users, but the record will inform future legislative proposals affecting Section 309(j) auction design.

The aggregate policy picture heading into the second half of the decade is one of constrained supply and sustained demand. Carriers have spent more than $265 billion deploying spectrum acquired through FCC auctions, and they face growing mid-band gaps as 5G traffic loads intensify. The DoD-commercial conflict over 3 GHz shows no near-term resolution. Auction 113 will provide a revenue and market-signal data point, but 200 AWS-3 licenses spread across three sub-bands do not substitute for the contiguous mid-band blocks carriers need. The pipeline beyond 2027 depends heavily on NTIA study timelines and interagency coordination outcomes that Congress has not yet been able to legislate around.